Uber Freight and Aurora started a partnership to pilot autonomous technologies at the beginning of 2020. (Business Wire)

Stay up to date with the latest transportation news by receiving TTNews directly in your email. ]

Uber Freight and Aurora Innovation announced on June 25 that they are launching a pilot program to give carriers early access to more than a billion miles in driverless deliveries.

The service, called Premier Autonomy by the companies, is designed to give carriers an early and streamlined way to purchase and deploy autonomy capabilities. The initiative aims at increasing the use of autonomous trucks by integrating the Aurora Driver technology into the Uber Freight platform. This is the latest evolution of a collaboration between the two companies in order to integrate and deploy automated technologies.

Uber Freight CEO Lior Ro said: “Uber Freight, Aurora, and other companies see a tremendous chance to democratize autonomous trucking for carriers of all sizes. This will enable them to generate more revenue, scale up their fleets, and strengthen their bottom line.” “Autonomous trucks make moving goods more efficient. This industry-first program helps facilitate and accelerate the use of autonomous trucks by our carriers.”

Uber Freight ranks No. Transport Topics Top 100 List of North America’s largest for-hire carriers ranks Uber Freight No.

We are thrilled to announce @uberfreight is one of our launch clients for driverless hauls scheduled for EOY. We’re launching Premier Autonomy – a program that reserves over a billion miles of driverless travel for Uber Freight carriers until 2030.

Uber Freight and Aurora started partnering in order to pilot autonomous technologies at the beginning of 2020. The Premier Autonomy Program builds on the insights gained since then about the effective and autonomous transportation of goods, , the companies said.

Through the program, Aurora provides early access to autonomous delivery to participating Uber Freight carriers until 2030. Uber Freight is Aurora’s first customer on its Dallas to Houston freight route.

“We have had a long-term partnership with Uber,” said Zac Andréoni, vice-president of business development at Aurora. “We hauled the first commercial trailer in 2021 with Uber Freight. This is a long-standing relationship, and this represents a real evolution of it into something bigger. We’re very excited about it.”

We’re working with @aurora_inno on democratizing driverless trucks

Premier Autonomy is an industry-first program that provides Uber Freight carriers with access to +1 Billion of Aurora’s driverless mile to Uber Freight carriers until 2030.

Aurora said that the size and density of Uber Freight’s network makes it ideal for autonomous trucks deployment. It’s no secret that the market for freight is in a recession. There is overcapacity, the prices are down, and costs are on the rise. The promise of AV, Andreoni said, is to deliver a supercharged asset which can run more efficiently for hours beyond service. “It’s a pretty compelling proposition.” If you’re a carrier in the middle market and have been wondering how to get it, now you can.

Aurora will continue to move loads for Uber Freight over the short-term, with the ultimate goal of decoupling itself from the asset side.

Andreoni stated, “We are still pursuing the commercial launch of our driverless service by the end this year. We expect to be able to transport driverless for our clients after that date as a third party carrier.” “We’ll own assets and operate them for our clients as any third-party carriers would. The economies will reflect this.” But that’s a temporary model.”

Andreoni explained Aurora’s long term model, which revolves around carriers buying an autonomous vehicle asset (from one of its manufacturing partners) and subscribing Aurora technology.

“It’s going be an interesting experience — it’s different from owning a vehicle today,” he said. “This program will prepare them for the ownership experience that we expect to begin in ’26 or 27. It will take some time to prepare or onboard them. We need to make sure their network is ready.”

SPA reported that the National Cybersecurity Authority (NCA), a government agency, attributed the Kingdom’s rise to its efforts both locally and internationally.

The Global Cybersecurity Forum is one of these initiatives. It provides a global platform for dialogue on cybersecurity issues. The GCF Institute also fosters international cooperation in this vital sector.

It stated that the establishment of the Gulf Cooperation Council Cybersecurity Ministerial Committee (GCC Cybersecurity Ministerial Committee) and the Council of Arab Cybersecurity Ministers – both spearheaded Saudi Arabia – signifies the commitment of the Kingdom to regional and pan Arab cooperation.

The Chairman of the Board of Directors of the National Cybersecurity Authority, Dr Musaed Al-Aiban, congratulated Saudi Arabia’s leadership for this achievement. He said that it was a confirmation of Saudi Arabia’s leadership in international cybersecurity, and a testament to the Saudi Vision 2030.

Al Aiban attributed this success to His Royal Highness Prince Mohammed Bin Salman bin Abdulaziz Al Saud Crown Prince and Prime Minster, whose vision has made the Kingdom a global leader in many fields.

Al Aiban stressed the strategic development of cybersecurity in the Kingdom, guided under Vision 2030.

He said that this development encompasses security and growth, with an emphasis on both domestic as well as international dimensions.

He said that the Saudi model is a pioneering example in this field and has attracted international emulation.

The Saudi Information Technology Company (SITE), which is its technical arm, was also established.

The SPA report stated that it has also conducted cybersecurity drills with over 40 countries to demonstrate its commitment to international cooperation.

The NCA added that domestically, it prioritizes cybersecurity through regulations and partnerships with industry stakeholders as well as targeted initiatives.

In 2021 Genius Sportsannounced the acquisition of Spirable. Spirable is a maker dynamic ads for social media, which allows, for example, live betting odds can be updated within display ads on Facebook. Genius and the executives of the startup are involved in a dispute over earn-outs. These incentive payments are increasingly used in the tech industry, and they’re causing lawsuits.

The company was excited about the potential of its expanding tech, which included Spirable. This would allow it to compete with leagues and sportsbooks. Steve Bornstein, the head of Genius North American business , said that in late 2021, “we’ll have an opportunity to really push forward in terms of technology, integration, and integration when you take all the assets of Genius Sports including Second Spectrum, and Spirable along with the gaming businesses.”

Spirable was a highly sought-after target. Its client list included Coca-Cola and DraftKings. Genius paid $37.5m cash for Spirable. The company was founded in Cork, Ireland in 2014 by brothers Dave and Ger o’Meara. Genius’ premium for the company is a testament to the excitement surrounding its technology. Spirable, according to regulatory filings, had revenue of PS2.8m and a net loss in 2021 of PS2.1m, which is about $3.8m and $2.8m, respectively. Genius agreed to earn $17.5 million for achieving technical targets and retaining executives after the merger. Documents filed in a U.K. suit between the O’Mearas, their VC investors, and Genius Sports show that Genius Sports also agreed to earn $17.5 million if they retained executives following the merger.

According to a paper authored by six Jones Day lawyers earlier this year, the use of such sweeteners for buying tech companies has increased sharply in venture capital. Earn-outs will be used in 21% of acquisitions for non-life science firms by 2022. This is up from 13% five years ago, according to law.

The Jones Day newspaper reported that “the use of earn-out clauses, which buyers and vendors often use to bridge different views of value,” is on the increase. “Lawsuits between buyers & sellers have also increased.” Sometimes the parties dispute if an earn-out clause’s performance target has been met at all… [or] that the buyer intentionally slowed down progress to keep the goal out of reach.”

The dispute between Genius vs Spirable seems to have a little of both.

Spirable executives claim in the lawsuit filed in November 2022 that Genius had already sought to undermine the earnouts due to Genius stock having lost about 75% of its original value. This led to a mandate for Genius to cut costs and save money. They claim that Genius executives had earlier in the year stated that some targets were met, but then changed their tune and refused to provide Spirable with resources to meet those targets. Spirable claims that Genius only fired enough executives to fall below the threshold needed to trigger executive retain-outs. This, they claim, also deprived Spirable’s ability to meet other earn-out goals.

In the complaint filed with the U.K. court, Spirable executives said that the defendant had tried to reduce the total consideration due to the Sellers in any way possible. “While the Defendant might consider that it made a bad deal due to the economic conditions that followed the acquisition of the company, that does allow them to avoid their contract obligations.”

David O’Meara refused to comment via email, and said that the other plaintiffs – his brother and VC firms Frontline Ventures & Smedvig Capital – also declined to comment.

Genius has not responded to many requests for comment.

Genius’ response to the court argues that its initial $37.5m was money badly spent.

“The acquisition was a failure.” Genius stated that the Defendant wasn’t impressed with the output received from Photospire, referring to Spirable under its original legal name. “Photospire employees were slow to grasp [Genius Sports’] technology and made slow progress with their various projects. Simultaneously they increased the demands on [Genius Sports’] resources and displayed an inappropriate focus on achieving Earn-Outs.

Genius stated in its filing that Spirable’s deal included five earn outs, of which two were revenue-based. These were missed but not disputed. According to filings from both parties, there is a heated dispute over the meaning of the language relating to the timing and requirements for the three earn-outs in question.

Jones Day says that’s not uncommon. The experience teaches us that the language used can have a huge impact on both parties in the event of a lawsuit. This change in control of the business, along with the competing incentives between the buyer and seller creates an environment ripe to disputes.

According to court documents, the dispute between Genius, the Spirable cofounders, and their VC investors continues for now. Arbitration between the two parties failed in spring. Now, discovery is underway. Witness statements are expected, and eventually a trial.

In an interview with Business Insider Paul Marino, Chief Revenue Officer at GraniteShares, highlighted that the cybersecurity industry is robust. Despite market fluctuations the sector is well-positioned to provide consistent returns to investors. GraniteShares, a firm that manages and invests assets totaling $5.2 billion, is a significant player in the investment world.

Resilience in the face of market volatility

Comparatively, cybersecurity companies rarely see a decline in demand. The private sector and government prioritize the secure storage of vital data, such as medical and financial records, in cloud-based systems. The Data Breach Report by the Identity Theft Resource Center highlights the importance of this need. It reports thousands of cybersecurity attacks with nearly 343 millions victims worldwide. Marino said, “This will continue to be a problem as long as we put data in the cloud.” Cybersecurity is a non-negotiable expense for companies. “Every single company must protect their data as well as their clients’ data.”

The cybersecurity sector is not fazed at all by volatile markets. Government entities continue to work to protect sensitive information amidst increasing cybersecurity attacks, geopolitical conflicts, and tensions. Geopolitical tensions can often force companies to retreat. You can never retreat from your security system. “You may even dig down when the going gets tough,” Marino added. He also stated that the frequency of cyberattacks by governments and foreign entities requires significant investment in cybersecurity measures.

Cybersecurity Investment Opportunities

Marino recommends four cybersecurity stocks to investors who want exposure to this resilient sector. These stocks are all part of the GraniteShares Nasdaq Disruptors ETF.

CrowdStrike Inc. (Nasdaq CRWD),

CrowdStrike, a leading cybersecurity company, uses AI and threat intelligence for ultra-accurate detections of enterprise risks in the areas of identity, data and cloud storage. The stock has risen over 58% in the year-to date (YTD) period, closing at $386.76 June 25. CrowdStrike’s annual recurring revenue (ARR), which ended April 30, grew by 33% YoY to $3.65 Billion, with a net addition of $211.7 M in ARR during the quarter. The company’s cash flow increased to $322.5 millions, which is 35% of the overall revenues of $921.25 million, an increase of 33% YoY.

In the quarterly earnings release George Kurtz, CrowdStrike’s President and Chief Executive Officer, highlighted the company’s competitive advantage. He said, “The Falcon platform’s differentiated architectural design creates a wide moat of competitive advantage and uniquely enables CrowdStrike’s to solve the biggest cybersecurity, data, and IT problems in the industry. Customers of all sizes are standardising the Falcon platform in order to achieve better security outcomes.” CrowdStrike’s CFO Burt Podbere said, “The CrowdStrike Team delivered another exceptional quarter, driven by strong execution as customers consolidate on Falcon platform.”

During the third quarter, CrowdStrike announced new innovations in cloud and data security and strengthened partnerships with Amazon Web Services and Google Cloud. These partnerships aim to improve cybersecurity consolidation and minimise breaches within multi-cloud environments. CrowdStrike has also partnered up with Nvidia for the delivery of the chipmaker’s AI-based computing services via the CrowdStrike XDR platform. The management expects Q2 revenues to range between $958.3 and $961.2 millions.

Zscaler (Nasdaq: ZS)

Zscaler is a cloud security specialist, focusing on zero trust connectivity. reported revenue growth of 32% YoY to $553.2 millions for the quarter ending on April 30. This was driven by increased client interest in its Zero Trust Exchange Platform. Zscaler CEO Jay Chaudhry said, “We delivered a quarter that was driven by increasing customer interest in our Zero Trust Exchange Platform.” As threat actors continue to exploit firewalls, Zero Trust security is a top IT priority. An increasing number of businesses are adopting our platform.

Zscaler stock has increased by over 11% during the last month. It closed at $182.52 in June. The company has been active in acquiring other companies to enhance its capabilities. It acquired Avalor Technology in order to improve AI innovations through the integration of its data repository with Avalor’s Data Fabric for Security. This allows proactive vulnerability tracing. Zscaler also acquired Airgap Network in order to combine Airgap’s agentless segmentation with its Zero Trust SD WAN, enhancing Zero Trust for IoT devices, critical infrastructure, and critical infrastructure.

Zscaler has also added a new AI assistant to its Zscaler Digital Experience Service, ZDX Copilot. This assistant can quickly evaluate and harness knowledge from more than 500 trillion data points. It provides valuable insights to IT Operations, Service Desk, and Security teams. Zscaler’s management expects revenue to range between $565 million and 567 million for the next quarter.

Fortinet (Nasdaq : FTNT).

Fortinet’s stock has grown significantly in the past five years. It closed above $58 on Friday, June 25. The global leader in networking cybersecurity reported an increase of 7.2% YoY in revenue to $1.35 billion during the quarter ending March. Management expects billings will rise to $1.55billion in the next quarter despite a 6.4% YoY decrease in billings. Revenue guidance is between $1.375billion and $1.435billion.

“We are diligently executing a strategy to leverage our size, go-to market capabilities, customer-first approach, and engineering expertise in order to capitalise the fast-growing Unified SASE markets and Security Operations,” said Fortinet’s CEO Ken Xie. He described the Unified SASE as the most comprehensive offering in the industry. It leverages AI innovation and product integration within the FortiOS operating systems.

FortiAI is the first IoT Security Generative AI Assistant that Fortinet has deployed across its networking and security product lines. This assistant supports customers across over 30 languages. The company announced the acquisition of cloud security firm Lacework. This deal is expected to close in the second half of this year. This acquisition will integrate Lacework’s CNAPP (cloud native application protection platform) into Fortinet’s Unified SASE, providing clients with a comprehensive AI-driven cloud-security platform.

Palo Alto Networks (Nasdaq: PANW)

Palo Alto Networks shares have risen over 11% in value YTD and reached above $322 last week. The cybersecurity giant reported a 15% increase in total revenue YoY to $2 billion. GAAP net income also increased YoY from $107.8 to $278.8 millions. Dipak Golechha is the CFO at Palo Alto Networks. He said, “We have been disciplined in our execution and invested in go-to market and innovation.” “We delivered consistent and profitable growth in Q3 again and look forward to executing on our strategic goals and financial target as we close the year.”

Nikesh Arora, CEO of the company, stressed the long-term platformisation strategy to address the increasing sophistication of threats. Palo Alto Networks is a leader in developing solutions to counter AI-based cyber threats. It has recently launched products that secure AI from the start. Precision AI, its proprietary offering, uses machine-learning, deep learning and generative AI in order to protect networks and infrastructure.

Palo Alto Networks strengthened its partnership with Accenture in May to help companies adopt AI safely. This partnership combines Palo Alto Networks Precision AI technology with Accenture’s secure generative AI service, strengthening clients’ AI environments through the AI lifecycle. The company also partnered IBM to deliver AI powered security outcomes, streamlining operational, halting threats and accelerating incident resolution. This collaboration includes the acquisition of IBM’s QRadar SaaS and migration of QRadar SaaS customers to CortexXSIAM, Palo Alto Networks next-gen security operation platform with advanced AI-based threats protection capabilities.

Palo Alto Networks anticipates total revenues of between $2.15 and $2.17 billion for the next quarter. This represents a YoY increase of 10% to 11%.

Disclaimer: Our digital content is only for informational purposes and does not constitute investment advice. Before investing, please do your own research or seek professional advice. Market risks can affect your investment and past performance does not guarantee future returns.

Venture capital investments in crypto continued to rebound in the second quarter, with a total $3.2 billion invested during the period — up 28% compared to $2.5 billion in the previous quarter, according to Galaxy Digital latest research report.

The report also identified a 94% quarterly surge in median pre-money valuation, which rose to $37 million from $19 million in the first quarter.

Galaxy noted the second quarter’s median pre-money valuation is the highest since the fourth quarter of 2021 and represents an almost all-time high. It attributed the surge to a more competitive market, giving companies greater negotiation leverage in deals.

Meanwhile, the second quarter median deal size grew to $3.2 million from $3 million, up 7% after remaining largely steady for five quarters. Deal count fell to 577 in the second quarter, down from 603 in the first quarter but up from less than 400 in the fourth quarter of 2023.

According to the report:

“Despite a lack of available investment capital compared to previous peaks, the resurgence of the crypto market… is leading to significant competition and [FOMO] among investors.”

The report highlighted a positive shift in crypto venture capital sentiment, buoyed by a nearly 50% year-to-date rise in Bitcoin and Ethereum prices. If the trend continues, 2024 will have the third-highest investment capital and deal count numbers after the bull markets of 2021 and 2022.

However, the report also noted that despite Bitcoin experiencing a significant rise since January 2023, venture capital activity has not kept pace, trading well below the levels seen when the flagship crypto last traded above $60,000 in 2021 and 2022.

The divergence is attributed to several factors, including crypto-native catalysts like Bitcoin ETFs and emerging areas such as restaking and Bitcoin Layer 2 solutions. Additionally, pressures from crypto startup bankruptcies, regulatory challenges, and macroeconomic headwinds, particularly interest rates, have collectively contributed to the breakdown.

Other data and trends

Specific project categories led fundraising — including Web3, which brought in $758 million or 24% of all capital. Infrastructure brought in over $450 million (15%), trading and exchanges brought in under $400 million (12%), and Layer 1 brought in under $400 million (12%).

Bitcoin Layer 2 networks continued to see significant investments of $94.6 million, up 174% on a quarterly basis. Galaxy said “investor excitement remains high” around the possibility of composable blockspace attracting DeFi and NFT projects to Bitcoin.

US companies dominated VC investment, attracting 53% of all capital and 40% of deals. Galaxy said US dominance exists despite regulatory change that could cause companies to leave the country and warned policymakers to be aware of their impact.

Early-stage firms received about 78% of capital, while late-stage companies received 20% of all capital. Galaxy said that larger general VC firms have left the sector or scaled down their activity, reducing the ability of later-stage startups to raise money.

Helsinki-based OpenOcean has closed a EUR3.9M financing round led by B2B, an early-stage venture-capital firm in Europe.

The funding round was led by Miki Kuusi, Marianne Vikkula, and Ilkka Paananen, from Wolt. Robert Gentz, from Zalando and Lifeline Ventures were Droppe’s current investors.

Tom Henriksson is OpenOcean General Partner. He says: “Through Droppe’s Source-to Order platform, buyers have the easiest way to order, source and manage products that are essential to their operations.”

Droppe is more than an online distribution channel for brands. It offers a scalable system for managing orders and a powerful data engine to deliver actionable insights about matching demand and supply. This helps brands understand how they can expand their market share, and enter new markets in Europe.

“Droppe’s strong founders have proven their ability to develop an online product that can be used by both small and large companies in Europe. We are proud to be able to support Johannes and Henrik on their next journey.”

A source-to-order platform

Droppe, founded in 2020 by Johannes Salmisaari & Henrik Helenius has developed a Source to Order platform for businesses. Droppe anticipates that 80 per cent of all B2B sales by 2025 will be done online.

Message from our partner

The platform is designed to meet the digital preferences of today’s buyers, allowing them to easily source, order and manage supplies such as safety gear, workwear, paper products and packaging materials.

Droppe allows direct supplier-to customer transactions, eliminating the need to store, repackage, and other logistics associated with moving products from brands into businesses.

This streamlined approach increases efficiency and supports the creation of shorter, more sustainable supply chains throughout Europe. Droppe claims that businesses can achieve their sustainability goals and contribute to a more sustainable future through its platform.

Over 150 leading European brands, specialising in safety products, workwear, packaging, and paper, have adopted Droppe’s Source-to Order Platform as a strategy to capture and expand the growing online market.

Droppe’s Source to Order platform is used by 150 European brands that specialize in safety equipment, paper products, packaging materials, and workwear.

Capital utilisation

The funding will enable Droppe to achieve its mission of transforming B2B distribution by moving away from the traditional methods that have been in place since the early 2000s and towards a modern digitally-focused method.

Salmisaari, the co-founder of Droppe, says: “We are in a very exciting phase, both for the company and market. With increased adoption of technology and millennials taking on buyer roles, business purchasing decisions are changing.

“The culture is shifting away from transactions made with salespeople via emails, physical visits and phone calls to digital experiences that streamline the purchase decisions and enhance collaborative management and coordination for recurring orders.”

Droppe will use the funds to improve its platform and meet online customer expectations for B2B clients. They also plan to hire new commercial talent in Helsinki, Cologne and other European cities to support their growing customer base.

Helenius, co-founder of Droppe, says, “The funding will help Droppe expand our database of suppliers and products, as well as their technical product and standard information. This will allow buyers to source and order products more efficiently and objectively.

Droppe will also focus more on supporting procurement and operations teams in Europe, helping them to manage the purchasing of their operation supplies, giving them greater control over their operation.

“We’ve seen a need for such a platform and are excited about expanding our offering.”

Madrid-based venture capital firm Seaya has closed Seaya Andromeda fund, Southern Europe’s first Article 9 climate-tech fund, at €300M. The fund’s limited partners include Iberdrola, Nortia, Santander, BNP Paribas Group, Next Tech Fund, and Bpifrance.

Carlos Fisch, partner at Seaya, says, “In addition to investors that can provide capital, there is a need for experienced investors with a proven track record who can support startups navigating the growth challenges in this space.”

“Since we started investing, we have backed 12 climate tech companies and have successfully exited three of them: Wallbox, RatedPower and Ecoalf.”

This new fund brings Seaya’s total assets under management to over €650M, making it the largest VC investor in Spain. ‘Seaya Andromeda’ intends to invest in 25 climate-focused portfolio companies before the end of 2027.

Accelerating the growth of startups

Seaya, with twelve years of climate tech experience, has launched ‘Andromeda’ to invest in companies focused on energy transition, decarbonisation, sustainable food value chains, and the circular economy.

Pablo Pedrejón and Carlos Fisch lead Andromeda as Investment Partners. The fund, adhering to SFDR’s Article 9, ensures that all investments have a positive impact on society or the environment.

– A message from our partner –

Pedrejón says, “Deep-tech climate entrepreneurs face a unique set of challenges compared to software-tech entrepreneurs. Climate-tech companies must translate research into a working product, bring it to market, and then scale it.”

“This long journey requires different kinds of support than what is typically provided to software startups. This is why there is a need for Series B and B+ investors that help climate tech startups bridge the ‘valley of death’ – the gap from initial development to deployment at scale.”

Seaya has already made its first five investments from the Andromeda fund into impact tech companies, including Recycleye, an AI-driven robot for sorting recyclable waste, and 011h, a construction firm reducing CO2 emissions by 75 per cent.

To back 25 startups by 2027

Seaya Andromeda is Southern Europe’s largest ClimateTech VC fund, managing €300M AuM and focusing on growth. It is part of Seaya, a European and Latin American VC platform with offices in Madrid, Barcelona, and Mexico City.

Seaya’s new fund will invest between €7M-40M as a first cheque and retain capital for follow-ons. It plans to make 25 investments by the end of 2027, including around five more deals this year.

Seaya, founded in 2013 by former private equity investor Beatriz González, is a female-founded venture capital firm. González’s first sustainability-focused investment was in Ecoalf, a recycled clothing line, in 2012.

Seaya Ventures has since invested in seven more sustainability startups, including Clarity.ai, Biome Makers, RatedPower, Samara, Crowdfarming, Descartes, and Wallbox, which went public on the NYSE in 2021.

Founder and Managing Partner, González, says, “From day one we were focused on impact and climate. We have a strong technological background in this space.”

“We started in 2012 backing climate tech companies and have successfully guided three of them right through to exit. We have 12 years of experience in this space and we can bring this knowledge and expertise to founders through this specialised vehicle.”

Seaya Ventures invests at the Series B+ stage in companies from the UK, Denmark, the US, and Spain.

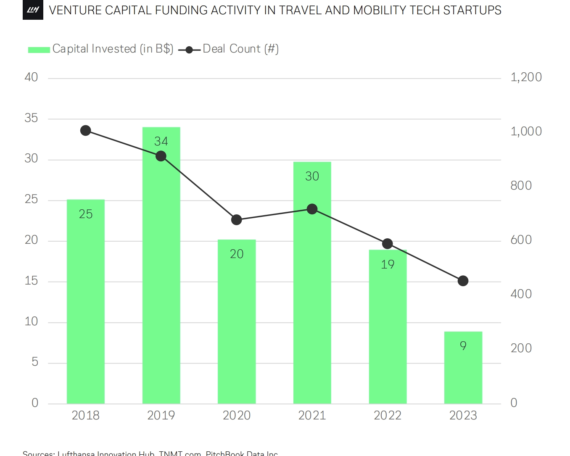

Despite a decline in VC funding, corporate investments in travel and mobility are still strong.

The latest “Travel and Mobility Tech Sector Attractiveness Report”, from Lufthansa Innovation Hub, provides an in-depth study of investment activity among 60 travel and Mobility corporations from 2018 to 2030.

The report highlights notable trends and investment priorities for aviation, ground transportation, hospitality, and on-line travel, providing insights into how these sectors navigate changing market conditions and economic challenges.

The report highlights a sharp drop in venture capital (VC), investment in travel and mobility startups in 2023. This fell to less than 10 billion dollars, less than a third of the peak in 2021.

This decrease is attributed by VC firms to the rising cost of capital and global interest rates. Despite the downturn in the industry, the need for innovative ideas persists.

The report also highlights that, in contrast to the VC landscape, corporate investment in travel and mobility has shown resilience. Despite a sharp drop in investment in 2020 due the pandemic. Investment levels rebounded in both 2021 and 2022 to reach pre-pandemic levels. In 2023, however, the economy experienced a slight decline, owing to broader economic uncertainty.

While VC funds have declined, corporate investment remains robust. AI and Machine Learning remain key investment areas reflecting their transformative power across the industry.

Sector-specific Trends

The report categorises investments into four main sectors: aviation (air and ground), hospitality (hotels), and online travel.

Key Findings include:

Aviation and ground transportation: These sectors account 60-70% of annual deals. Stability is achieved by corporate venture capital funds, structured investment strategies and asset-heavy industries. Over 180 deals have been made in aviation by major players including Boeing’s AEI, Aerospace Xelerated and JetBlue Ventures.

Online travel and hospitality: These industries are less involved in investing, with fewer institutionalised fund. Investments are often opportunistic and dependent on financial availability.

Sustainability and operational efficiency. Regulations and public scrutiny are driving a focus on sustainability in aviation and ground transportation. Investments are aimed at enhancing operational efficiency through digitalization and technological innovation.

AI and Machine Learning Investments

The report shows that Artificial Intelligence and Machine Learning (ML), which are at the heart of all sectors, have attracted two-thirds (or more) of investment deals in 2018.

Key applications include

Autonomous driving Investments in computer vision systems and LIDAR for autonomous vehicles.

Drones and robotics: Automating manufacturing processes, and refining delivery system

Predictive Analytics: Optimising process and increasing operational agility.

Customer Support – Enhancing interactions by using natural language processing and large languages models.

The continued focus on AI highlights the role it plays as a fundamental driving force for future growth and innovation within travel and mobility.

Shifts and shifts in hospitality, online travel

Lufthansa Innovation Hub data shows that hospitality companies have expanded their boundaries beyond the traditional, investing in startups that offer tours, experiences and travel-related products. This trend, partly driven by the pandemic and aimed at diversifying revenue streams and enhancing customer experiences, is partially driven. Investment activities slowed down in 2023, due to inflation, rising energy prices and staff shortages.

Online Travel Agencies have pursued expansion strategies. Notable acquisitions include Trip.com’s acquisitions of Travix and Despegars acquisitions of Best Day Travel. Asian investors have been active, with AirTrip and Yanolja among the leading investment companies.

Emerging Trends in Electric Mobility

Ground transport investments are increasingly focused on charging infrastructure for electric vehicles (EVs) and battery swapping technology. Joint ventures such as Kakao Mobility, LG Unplus and TIER are supporting the UK-based Bonnet Platform.

Aviation sustainability investments are on the rise, with more than 30% of deals focusing on decarbonization. This trend is driven primarily by regulatory pressures, as well as commitments to reduce emission levels. For example, the International Air Transport Association (IATA) has set a goal of achieving net-zero emissions by 2050.

The report also notes the environmental impact of electric take-off and land (eVTOL aircraft) remains a topic of debate.

XI’AN — In a bustling freight terminal in Northwest China, rows of brand-new electric vehicles gleam in the noonday sun, while workers use forklifts and cranes to stack containers onto waiting trains.

This is a typical scene at the China-Kazakhstan (Xi’an) Trade Logistics terminal in Xi’an, Shaanxi province, the starting point of the ancient Silk Road. The freight terminal was launched in February to facilitate the operation of China-Europe freight trains, which are often referred to as the “steel-camel caravans.”

It was jointly launched by KTZ Express, a subsidiary of Kazakhstan’s national railway company Kazakhstan Temir Zholy (KTZ), and Xi’an Free Trade Port Construction and Operation Co Ltd. Its counterpart in Almaty is expected to be put into operation later this year.

Olzhas Aleibekov, deputy general manager of the Chinese branch of KTZ Express, said the terminal, located at a crucial logistics hub, can effectively alleviate customs congestion and enhance the stability of transportation times.

Trains traveling between China and Kazakhstan have to be transferred to different tracks at the border due to varying track gauges, a process that can take up precious time. Also, the customs clearance process can be complex, and in the past, this often took three to five days.

Located more than 3,000 km from the border, the new terminal provides solutions for both of these problems. When the trains are still at Xi’an, KTZ Express communicates with partners in Kazakhstan to pre-arrange containers and railcars based on the cargo, ensuring efficient transfers and timely delivery.

In addition, trains at the Xi’an terminal are prepared for customs clearance, which means the procedures can be completed within an hour of the train reaching the border in Northwest China’s Xinjiang Uygur autonomous region.

To date, more than 35,000 tonnes of goods have been transferred through the terminal in Xi’an.

With enhanced operational capacity, the delivery time between Xi’an and Tashkent, Uzbekistan, has been reduced to nine days from 13 days, and the combined rail-sea transportation across the Caspian Sea has been shortened from 20 days to 12 days.

“This terminal has facilitated more efficient cargo transportation between China, Kazakhstan, Central Asia and Europe,” said Aleibekov. “Particularly in light of disruptions to the Suez Canal and Red Sea routes due to escalating geopolitical tensions, the reliability of the China-Europe freight trains has been further proven.”

PFIT International Logistics Co Ltd in Xi’an was among the first group of beneficiaries.

Ma Dong, the company’s general manager, said that previously, the company relied on sea routes that took up to two months to transport seamless steel tubes to Baku, Azerbaijan. Now, by using the Xi’an terminal, the journey takes just 12 days, saving 800 US dollars per twenty-foot equivalent unit (TEU).

China was Kazakhstan’s largest trading partner in 2023, with two-way trade up by 32 percent year on year to reach 41 billion US dollars.

Trains speeding along rail tracks have become a symbol of international trade in the new era, just like camel caravans were in ancient times.

Since the first China-Europe freight train left Southwest China’s Chongqing municipality in March 2011, the trains have completed over 90,000 trips, reaching 223 cities in 25 European countries and over 100 cities in 11 Asian countries. More than 8.7 million TEU containers of goods were transported, valued over 380 billion US dollars.

Cross-border e-commerce companies are leveraging China-Europe freight trains to gain convenient access to affordable international delivery services.

So far, 27 companies in Xi’an have built 51 overseas warehouses across 24 countries and regions. The city’s cross-border e-commerce transactions exceeded 16.8 billion yuan (about $2.36 billion) in 2023, marking a 16.7 percent increase from 2022.

“Overseas customers can now purchase Chinese products and enjoy door-to-door service with just a few clicks of the mouse,” said Jumekenova Anita, a Kazakh entrepreneur who founded a cross-border e-commerce platform called Silkroad City Shop and built warehouses in Kazakhstan, Russia and Belarus.

“The terminal sets a precedent for multinational cooperation in the development of China-Europe freight trains,” said Yuan Xiaojun, general manager of Xi’an Free Trade Port Construction and Operation Co Ltd.

What are the main drivers behind the development of Europe’s healthcare market?

Geraldine O’Keeffe

Geraldine O’Keeffe: I have been working in this industry for over 20 years, first in a medical diagnostics company and then in investment banking, before moving into the investment side. When I started investing, there were a lot of small sub-scale companies scattered across Europe. We have fantastic science and innovation in Europe, with top universities and high-level research in each country, but we were lagging behind in terms of company creation and attracting investors.

Traditionally, European investors have been quite conservative, but that funding landscape has changed in the last five years, with more capital flowing into venture investing in Europe. I began my career with Life Sciences Partners, which was the first European venture firm to raise a dedicated €1 billion life sciences fund, but several others have since followed. LSP combined with EQT in 2022 and was renamed EQT Life Sciences.

Early-stage companies are now much better funded and no longer need to run clinical trials, innovate and develop technology on a shoestring. That means there are better companies coming through the ecosystem delivering better products.

Those dynamics transformed venture investing in European healthcare, but once companies reached commercial stage there were still relatively few specialist healthcare investors to follow up. LSP did not have the scale to target those commercial-stage enterprises, but EQT recognised a real opportunity in those mid-market buyouts and nascent commercial-stage businesses. That is a segment we are now focused on, which includes opportunities across pharma services, contract development and manufacturing organisations (CDMO), life sciences trials, diagnostics, medtech and speciality pharma across Europe.

Mark Braganza: The healthcare market has always been global from a product perspective and European companies have always played a critical part in that ecosystem. In addition to the scientific community there was also an incredible heritage in Europe in sectors such as industrial chemicals and high-performance engineering, which are core to medical products.

Mark Braganza

While the regulatory landscape has historically been fragmented across Europe, now the European Medicines Agency is embedded with a consistent cross-border structure for taking products forward. The recent implementation of the new Medical Devices Regulation also helps. There is still some jujitsu around pricing and strategy to launch products, but Europe has become more of a cross-border opportunity.

As the global industry has looked to increase efficiencies and access expertise, so supply chains and value chains have transformed. Given the innovation and strong management teams present in Europe, plus the support functions you need to bring products to market, we have seen an explosion of opportunity. The capital side used to be more difficult, but that has changed significantly in the last decade.

How is the need for capital, as well as the challenges around financing innovation, fuelling that opportunity set?

MB: Part of the challenge is that in Europe we have been very good at innovation, but what is just as valuable and has been missing is the support for developing new products. That is not a venture capital problem but a growth capital problem, and that segment has not grown meaningfully across Europe. We haven’t historically had people that understand the technical complexity of the healthcare space and pair that with the business-building capital that is required to build these healthcare services companies.

In the US, instead of having generalist investors supporting the growth of these services businesses, there is a growing crop of sector specialists that can help those businesses to scale. Companies often have real revenues and real profitability but need scaling support to figure out how to build their commercial infrastructure, geographical footprint and supply chain. That has been slow to develop in Europe.

GOK: Obviously, scientific advances lead to whole new treatment modalities, such as cell and gene therapy. There is a need for new technologies, and new manufacturing processes, new diagnostics and new tools to scale that up, and that is all gaining momentum.

At the same time, there is also a need for more near-shoring of component supplies and manufacturing, which is all going to help build this industry in Europe. As the technology matures, the costs of labour as a proportion of production costs come down, which shifts where people seek to source from.

The complexity of supply chains was highlighted during covid, and as concerns around supply chains continue, that creates more opportunities for the industry in Europe.

Additionally, some of the shifts in technology fundamentally change the way manufacturing is done. The historical scalability of manufacturing, where it was better to have one or two very large manufacturing facilities, doesn’t necessarily work with new product sets. Where you manufacture, how close you are to the patient, how you move those products around the globe and how you ensure quality and traceability across the supply chain has all changed. That feeds into new opportunities for smaller companies, because personalised medicine is less about large manufacturing facilities and more about addressing complexity and quality on a smaller scale.

Are there any other dynamics that are creating investment opportunities, and how do those vary across Europe?

GOK: Another example would be pharma services, because as clinical trials have become more complicated and our understanding of diseases has improved, we have seen consolidation in the contract research organisation (CRO) space and more specialist service providers cropping up. We have also seen huge advances in healthcare IT, moving from lots of ideas a few years ago to the emergence of robust companies today.

CROs are popping up across Europe because it no longer matters where a company is headquartered, and the same is true of healthcare IT. It is a whole new business model and one that we are seeing opportunities in.

MB: There have been waves of industries across Europe. We had these very strong engineering services businesses in the DACH region and great industrial chemistry across DACH, Northern Europe and the UK, with waves of scientific support services in Benelux. Those have now generated ecosystems of entrepreneurs that have had successful businesses and exits and have started services businesses to support others. There are pockets of expertise across Europe, but those services cross borders really easily.

It is worth noting that half of the healthcare market is about care provision, but that is not what we are talking about when we talk about healthcare investing. We view that part of the market as very local; we focus on products and services and getting those into people’s hands, because those businesses scale across borders.

How do you see Europe’s healthcare landscape evolving in the coming years?

MB: There may be a relatively immature ecosystem in Europe today, but market participants understand that things are maturing quickly. While a small number of parties have so far gone on to be global winners, the barriers have now come down.

Over the next five to 10 years, assuming there is capital to match the opportunity, we should see a growing number of European winners providing global services. They will become interesting to strategic acquirers and will exit to multinationals, but we will have this new engine of businesses with the freedom and capital to mature and become globally relevant assets.

Private equity doesn’t run businesses, but we can enable management teams, and there is now a phenomenal bench of experienced healthcare executives in Europe who have seen success. If we can match them to specific companies, we can help accelerate their growth trajectory. If we can help grease the engine for those companies, that experience is a win-win for everyone.

GOK: We believe Europe is finally coming to an inflection point. We have had the science and technology and the innovation, but we now have the capital sources to bring this forward so the industry can flourish. We can help those companies mature and get to the next stage.

What are the key challenges for European healthcare investors today?

GOK: Europe has always struggled with a fragmented market on the public side, where the focus is on local support for local companies. We have been waiting for markets to mature, but there have been scenarios where biotech companies would go public first in a local market and then do a secondary listing on the Nasdaq. If anything, that situation has worsened, because now companies list on the Nasdaq first and it has become even more difficult for European companies to IPO. That makes private capital even more important today.

MB: The other issue for the companies that we are investing in, where we need to be solving problems for management teams, is the fact that they need to scale cross-border if they are going to be able to continue to grow and compete effectively. Regulations have become clearer but there is more for management teams to do, with an element of cost that requires scale, and a significant element of complexity.

We spend a huge amount of time looking for niche leaders, which tends to mean talented management teams with experience in the industry who have found a solution for something that people have been struggling with. That may be selecting compounds, manufacturing them, moving them around or commercially launching them. But they have typically done that on a relatively small scale and to expand they need corporate infrastructure, with top-notch regulatory and compliance, and that can be a challenge.

Geraldine O’Keeffe and Dr Mark Braganza are partners in the EQT Healthcare Growth advisory team